We do a bit of business planning work here at Regional Strategic, Ltd. Our president, Mark Imerman, cut his teeth on business planning as a market development economist at the Iowa Department of Agriculture and Land Stewardship. It that role, he assisted farm operators and investors develop marketing facilities for alternative crops. It was a strategy pursued by the State of Iowa to reduce dependence on traditional row crops during the farm crisis.

In that role, he generally produced complete business plans:

- Business description and objectives

- Management qualifications

- Personnel biographies and job descriptions

- Sources of technical support

- Market analysis

- Competitive analysis

- Pro forma financial projections

- Investment and capital needs

At Regional Strategic, Ltd., however, we seldom get requests for the whole ball of wax. We primarily get contracts to do the market and competitive analyses. It is challenging and satisfying work. Every product, region, and delivery channel presents a different situation. All of these efforts are unique.

One thing we seldom see, anymore, is a full pro forma financial layout in small business development. This is true whether we are asked to help with small business planning or we are looking at plans done by others. Instead of detailed breakdowns of revenues, expenditures, and investment needs by month, we see rough annual estimates of total payrolls, start-up costs, production volume, and revenue.

This is unfortunate. The estimates might be well-informed and accurate, but the lack of detail is unfortunate, nonetheless. Annual estimates don’t match up revenues and expenditures as they occur. This is important, particularly in a small business startup. Without this, initial cash needs might be substantially underestimated simply because of mismatches between the accrual of expenditures and the realization of revenue. Annual estimates also hazard the risk of overlooking costs that might be incidental in and of themselves. These costs, in aggregate, can often be consequential. Missing them can result in material differences in overall estimates. There are often underestimation issues with startup costs, as well.

All of these factors increase the financial risk of business startup investors. They also increase uncertainty upon the part of potential lenders. This often results in elevated interest and insurance costs. In combination, these result in fewer small business startups in any given community. This reduces community income which reduces community tax revenues and impedes the improvement of community services. In short, they retard a community’s growth potential.

A five-year monthly pro forma financial layout encourages a business owner to walk through the first 60 months month-by-month. Properly set up, it will allow the investors and lenders to do what-if scenarios easily.

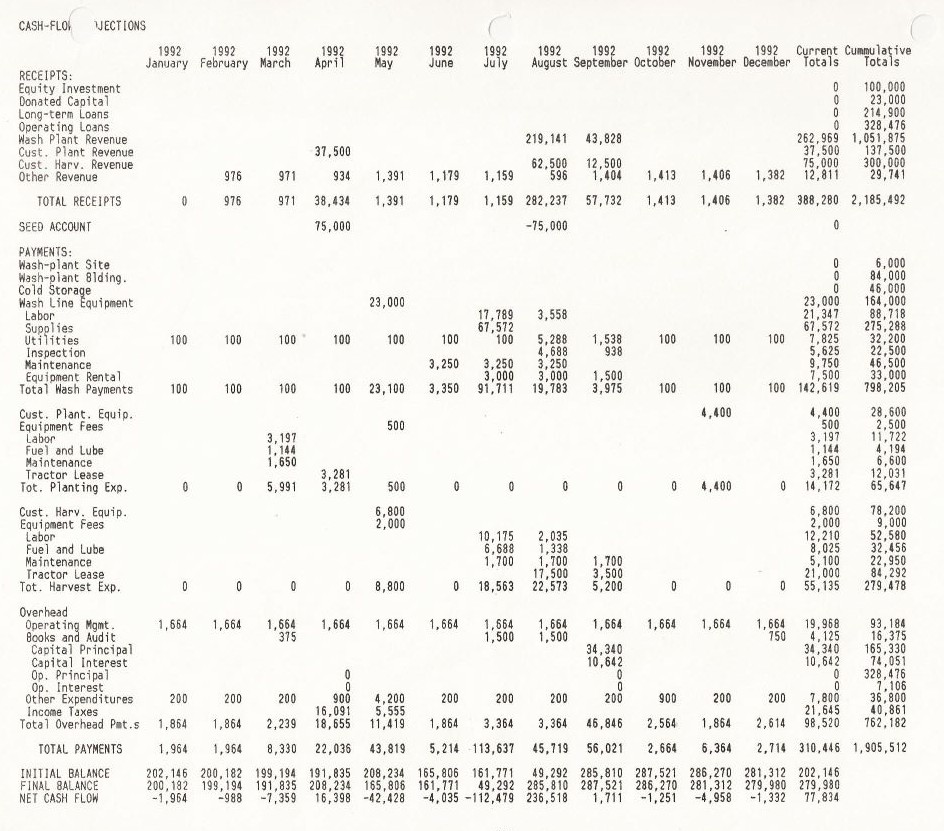

The table below is the fifth-year cash flow layout of one of Mark Imerman’s first business planning exercises. This particular plan specified financial requirements for a contract service provider engaged in planting, harvesting, packaging, and selling an alternative perishable food crop in Iowa. The spreadsheet analysis was set up with a single sheet of annual assumptions regarding acreage, service costs, output, waste, and revenues. Numbers in the cash-flow layouts were calculated from these assumptions. As a result, basic changes could be made concerning expected costs, acreages, yields, and sales prices, and those changes would automatically change the annual cash-flow layouts, which, in turn, would ripple through the annual operating and balance statements.

Pro forma financials are powerful tools. They result in better informed and prepared business owners, more confident investors and lenders, and increased potential for business growth within a community.

This was a relatively small investment project. It required a direct investment of about $130,000 and long-term loans of about $220,000 at the time. Given inflation, that is nearly equivalent to a total investment of $700,000 today. Long-term loans to accomplish this investment would likely have not been available in the absence of the pro forma analysis.

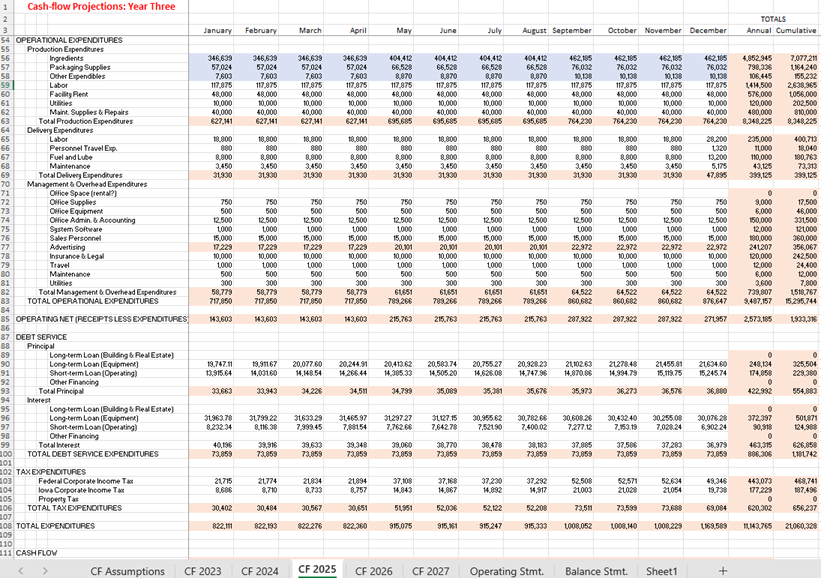

The second table shows a more recent example. It represents a potential frozen food manufacturer serving a limited geographic market in the upper Midwest. Figure Two shows the third-year expenditure portion of a five-year pro forma. Along the tabs at the bottom of the screen shot, you can see sheets for five years’ cash flows, balance sheets, and operating statements. There is also an assumptions sheet that drives cash-flow calculations. Cash flow calculations drive operating statements and balance sheets.

A set-up like this allows developers and investors to walk through alternative scenarios. You can see that production expenditures increase across the year. This reflects a scenario where output is still growing as the initial investment matures. Delivery expenses do not grow on the same schedule as production expenses. This reflects the lumpiness of delivery investments. All of these things become obvious when working through monthly pro forma cash flow projections. They are easily missed in annual lump sums.

Overall, the more recent operation is larger than that represented in the first table. The more recent table is part of the projections for a $5,000,000 investment. Generally, Regional Strategic, Ltd. works with business planning projects with investments between $500,000 and $15,000,000. It is a market segment that almost always benefits from a rigorous estimation of expenses and revenues.